Pricing 101 - Understanding Energy Pricing for Residential and C&I - Part 1

What’s the price of using a light? A fridge-freezer? A TV? A production line? Invaluable, right? The modern world functions on energy. The industrial revolution was powered by electricity. 200 years later, it remains just as important, but the way we receive and pay for energy has changed quite a bit. From the consumer side, using and paying for energy is quite simple, but this hides a huge amount of effort that goes into the delivery and correct pricing of that energy. How does it actually work, and what are the challenges that energy retailers face when delivering prices? Welcome to Pricing 101, a series of blog posts which will answer every question you might have about the pricing of energy.

The first post in this series will explain briefly how modern electricity systems deliver power to the people, and where energy retailers fit in the new system. We will then explore the processes retailers go through to create the prices they offer.

In parts 2 and 3, we will break down the pricing process further into pricing for residential customers and pricing for commercial & industrial customers, looking at the challenges retailers face to create competitive pricing that still delivers enough margin.

Part 4 looks at the costs which drive electricity prices, focusing on the wholesale market and its factors. We will also examine future trends which could impact the cost of energy.

Finally, part 5 will look at other side of energy pricing: gas. Though many of the factors that influence prices are the same for both electricity and gas, gas is still a different market with unique considerations. This series will use "energy" and "electricity" interchangeably until part 4.

Understanding modern energy delivery

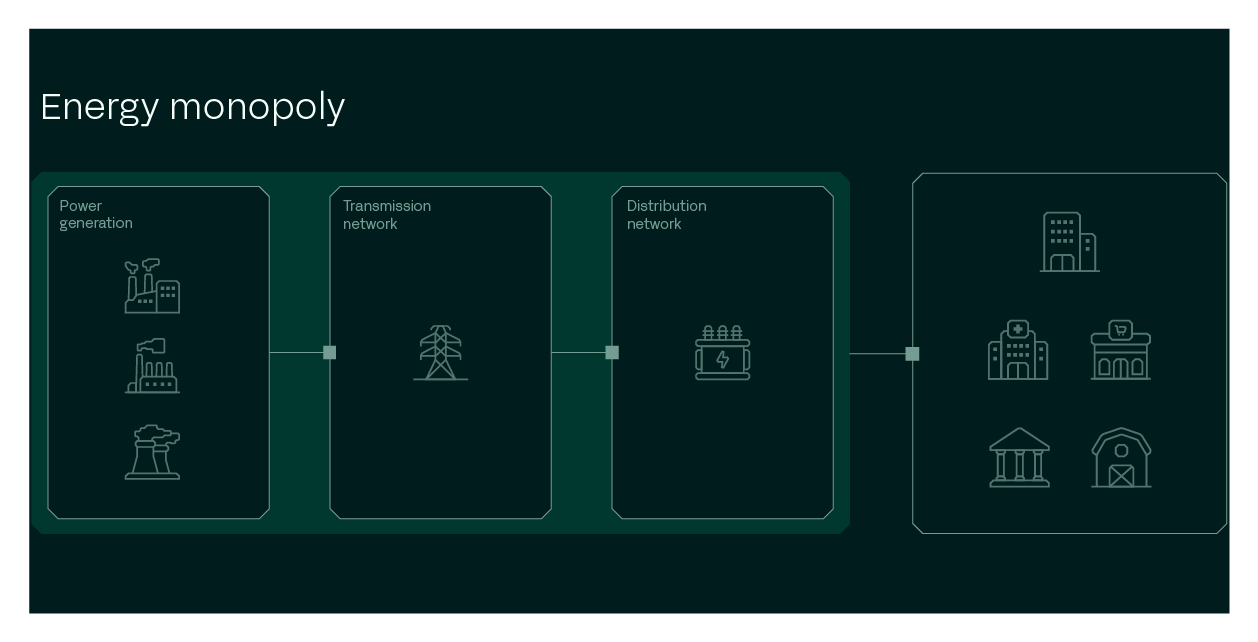

For a long time, pricing was an internal accounting exercise leaving customers little say over the sources or costs of energy usage. A single entity controlled the entire supply chain, from generation to distribution, forming a natural monopoly. They would examine how much energy was generated, what it cost to transmit and distribute, and how much a customer used, and then provide a bill including a pre-determined profit margin. In a lot of US states and countries worldwide, this is still the case. In this system, there is little transparency to how prices are calculated as the costs at each stage are known and handled by the same entity.

Liberalizing the energy sector

The first country to break with this traditional model was the UK, beginning with the Electricity Act in 1989. The UK broke up the energy monopoly, unbundling each part of the supply chain. The Central Electricity Generation Board was split into two power generation companies and a transmission business, National Grid Company, that retained monopoly control of transmission. Over the next decade, the power companies were further broken up and retail competition was introduced, eventually leading to the current system of separate generators, distribution companies, and retailers. However, there was no restriction on vertical integration with some utilities still operating across all parts of the electricity supply chain. Gorilla customer ScottishPower is a retailer but also operates distribution, transmission, and generation. The UK’s privatization set the standard for other countries to follow.

In the US, energy market design varies by state. Texas is the only state to fully embrace deregulation. California and Maryland were the first to experiment with the system, deregulating gas supply in 1995. Ohio was the first to deregulate electricity in 1996. Today around 27 states have deregulated gas, electricity, or both in some form. The US system is further complicated by states which have deregulated wholesale markets but do not offer retail competition. There are 7 wholesale markets operating in the US: CAISO, SPP, ERCOT, MISO, PJM, NYISO, ISO-NE, which cover both regulated and deregulated states.

At the core of modern energy pricing are two markets: retail, and wholesale. The wholesale market is where power generators sell the electricity they generate to suppliers, and retail markets are where suppliers compete to attract customers - both residential and commercial. The prices that a supplier can offer will be at the mercy of the prices offered on the wholesale market, which engenders intense competition to offer the best deals to potential customers. - or at least, this is the theory behind privatization.

Wholesale markets function based on marginal cost - the cost of producing the last unit of electricity. Marginal cost for generators will vary greatly depending on the type of power generation; renewables and nuclear have near zero marginal costs, while more traditional sources have to cover the costs of fuel. A wholesale market that covers the majority of its capacity needs with low cost renewable energy could still offer high prices to retailers if the remaining need is covered by expensive peaking power when demand is at its highest.

Changes in consumption & generation

Energy delivery is not the only process that has changed over the years: generation and consumption are different as well. A more accurate energy market diagram might look like this:

The rise of DERs, distributed energy resources, has had a big impact. Solar panels, wind turbines, and other small, private sources of energy mean that customers can now generate their own electricity and even sell it back into the grid in some markets. Battery storage has added resilience to the grid and helped enable the spread of renewable generation, providing a tool to manage intermittency. Patterns of consumption have also been affected by new technologies like electric vehicles (EVs), which draw much larger amounts of electricity and are often left to charge overnight. Typically, demand for electricity is concentrated in the evenings when people return from work, with demand falling sharply at night, but EVs, as well as the rise of remote working, have drastically changed this traditional pattern.

How people consume energy is important due to the way that utilities purchase energy from wholesale markets. Baseload capacity can be bought years in advance, but settlement in real-time will experience changes as utilities are forced to react to these new consumption patterns.

How retailers create prices

The primary services of an energy retailer are acquiring energy supply, calculating energy prices, delivering competitive prices to customers, and collecting payment. In most cases, they have no involvement in the actual delivery of energy, which is done by the generators and distributors. It would not be impossible to have an energy market without retailers and have customers buying directly from generators & distributors; it would simply be incredibly complicated. Retailers facilitate the final stages so that customers don’t have to.

In light of this, retailers need to make sure that their core services are done as well as possible. Pricing teams will be at the heart of retail operations, ensuring that the company is delivering the best possible rates to attract customers and still make a profit.

The pricing process typically involves the following steps:

- Cost analysis:

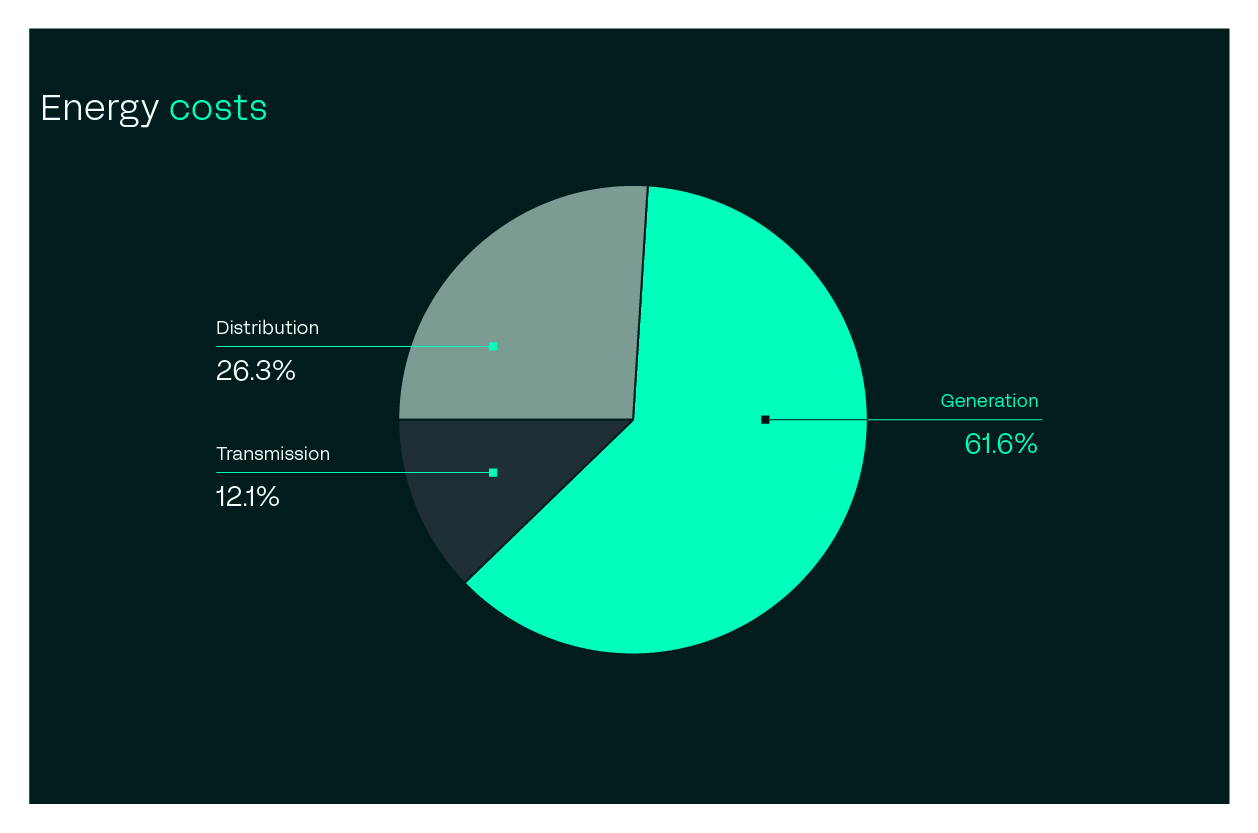

Energy retailers analyze their costs to determine the price at which they can sell energy to customers while remaining profitable. The primary cost of energy is the wholesale price, which is the cost of generation. The costs of infrastructure for transmission and distribution also need to be accounted for. The US Energy Information Administration calculated the following division of costs between each part

Once those costs are covered, retailers have to consider their own operational costs such as customer service and marketing. Finally, retailers need to include a profit.

- Market analysis:

How will prices change over time? What will demand look like? Energy retailers analyze the energy markets to understand supply and demand dynamics, regulatory and policy developments, and other factors that may impact the price of energy. Forecasting plays a key role here in predicting demand and keeping costs low.

Markets worldwide have undergone supply shocks over the past few years, driven by the war in Ukraine and inflationary pressures. The US was able to avoid the huge spikes in energy costs that much of Europe experienced thanks to the boom in fracking but retailers have still suffered from the uncertainty.

- Rate design:

Energy retailers design their rates to reflect the cost of energy and the associated delivery costs, while also meeting customer needs and preferences. This may involve offering different rate plans, such as fixed or variable rates, and incorporating other factors such as time-of-use pricing or demand response programs. Energy retailers work with risk premiums to factor in the risk of changing demand and unforeseen market events.

- Tax and Regulatory compliance:

Energy retailers must comply with relevant regulations and policies related to pricing, including those related to consumer protection, anti-discrimination, and transparency. Taxes will apply to every energy bill and there is a growing push for carbon taxes as well as fees for renewable energy investment, though these will vary heavily by state.

- Competitive positioning:

Finally, retailers have to consider the competitive landscape. Price is the overwhelming factor when it comes to choice of utility, and so an uncompetitive offer could have dire implications.

Processes will be similar for both residential and C&I, but the types of products available will differ, meaning there is some divergence depending on who is being sold to.

A variety of people and teams will be involved in this process, but the primary responsibility falls to the pricing team, which is typically composed of pricing managers and pricing analysts. The teams are required to balance a huge amount of data coming from disparate systems and sources. Typically, industry and market data will be fed into a pricing engine, along with data from an ETRM to enable pricing teams to produce accurate tariffs. Many engines also perform billing, combining tariffs with consumption data to determine how much customers owe.

The biggest problem for pricing teams? “Pricing Engines” are often just Excel spreadsheets or other legacy applications. They are not designed to integrate with modern data pipelines nor to handle hundreds of gigabytes of data for processing day in and day out.

The next post will look in more detail at the residential pricing, as well as the specific challenges that pricing teams need to face for B2C.

Read further

Gorilla launches a pre-billing calculation layer for I&C energy contracts

More than 90% of European energy executives claim their margin reporting is accurate – but new research reveals “Margin Confidence Paradox”