Understanding Proposals from the UK’s Review of Electricity Markets second consultation

The UK completed its second consultation on electricity markets on the 13th March, highlighting 4 key challenges that need to be addressed to continue progress on decarbonisation.

The UK has been at the forefront of implementing market-based mechanisms in the energy sector, pushing for private company involvement in providing electricity and gas. As part of a global movement for governments to move quickly towards net zero emissions, the UK is committed to sourcing all electricity from non-carbon sources by 2035.

To meet this goal, a number of government initiatives have been launched, including a review of the electricity markets in the UK. Starting in April 2022, the Review of Electricity Market Arrangements, or REMA, sought to solve inefficiencies in the current electricity market design. The second consultation phase of REMA has just released its findings, identifying 4 key challenges that will need to be solved, alongside a number of policy solutions for each challenge. We’ll take a look at each challenge and the policy proposals below.

The 4 Challenges

- Passing through the value of a renewables-based system to consumers

The first challenge is focused on the issue of marginal pricing in electricity markets, which leaves customers footing the bill for high and often fluctuating prices for gas generation, despite costs for renewable generation being significantly lower.

- Investing to create a renewables-based system at pace

The second challenge involves balancing the risk of investment in additional renewable energy capacity to ensure that the significant level of investment needed for 2035 is met. Transitioning to a renewable energy system requires significant upfront investments in infrastructure, including wind farms, solar panels, and the enhancement of the grid to handle distributed and intermittent power sources.

- Transitioning away from an unabated gas-based system to a flexible, resilient, decarbonised electricity system

The third challenge deals with security of supply. Renewable energy sources are intermittent and cannot be relied upon at all times, while battery storage is not yet advanced enough to mitigate this problem. While there are flexible low carbon electricity sources, the market does not currently offer enough capacity, particularly compared to the abundance of gas supply.

- Operating and optimising a renewables-based system, cost-effectively

The final challenge is about the operational aspects of a renewables-based electricity system. The unpredictability of renewable energy sources makes it challenging to balance supply and demand in real-time. This challenge focuses on finding cost-effective ways to operate and optimize the electricity grid under these conditions, particularly with regard to locational-based signals.

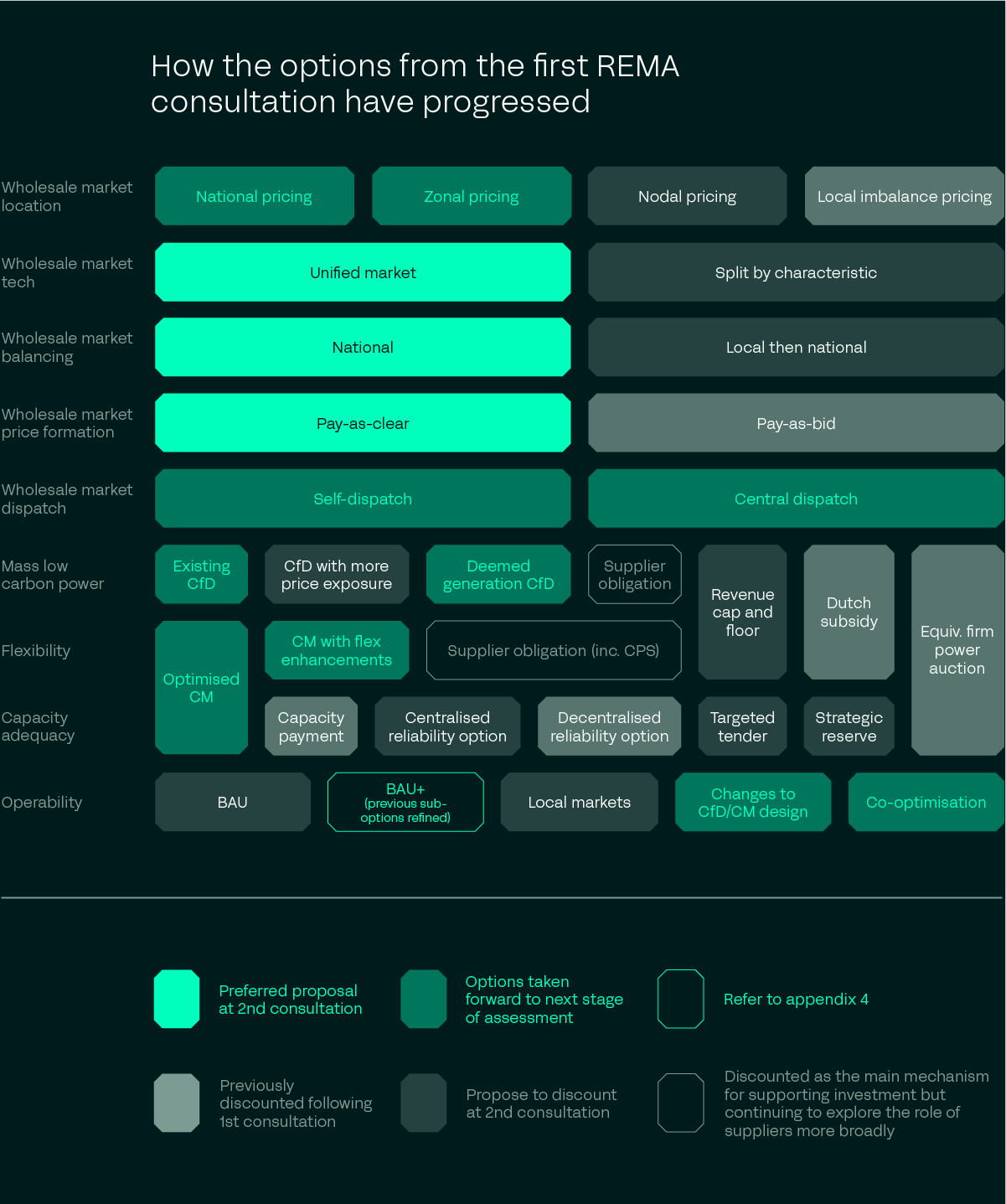

Policy Suggestions

As this is the second REMA consultation, a number of policy proposals have already been advanced and discounted, with more clarity on likely paths forward now available. It is not worthwhile to consider every single policy shown above in detail, and instead a high level summary will be offered.

Perhaps the largest impact in terms of proposals comes from the advance of locational pricing in the UK, with nodal pricing now being discounted as a solution. The primary option being considered is zonal pricing, which would lead to different wholesale prices for different zones across the UK. However, we don’t anticipate that “zones” will mean anything on the level of different prices per each grid supply point. The report itself makes reference to “a maximum of a dozen” pricing zones, for example.

The intention of locational pricing is not necessarily to pass on local savings to end consumers, but rather to improve the overall system efficiency:

“modelling shows that locational pricing under the form of zonal pricing could reduce the cost of running the electricity system in the region of c.£5-15bn over 2030- 2050”

Naturally, there is an expectation that savings of this amount are passed onto customers, with an estimate of between £25-60bn of potential savings for customers, but it is not certain that this will be provided by offering different prices to customers rather than through passing general lower system costs on. At the moment, both options are on the table, and retailers should certainly start to consider their capabilities around offering local prices directly to customers.

The Capacity Market (CM) has seen a big vote of confidence from REMA as the primary solution to delivering flexible, secure electricity supply. A minimum procurement target (known as “minima”) will be implemented to push investment in low carbon supply, with 55GW of short-duration flexibility targeted for 2035.

One almost unspoken development that emerges from the report is that gas is not going to go away any time soon. Though much is made of investment in technologies such as hydrogen power generation and battery storage to pave the way for further decarbonisation, it remains clear that gas will continue to back up renewable energy for the foreseeable future - though this will not come as a surprise to some, given the government separately announced more funding for gas very recently.

Contracts for Difference (CfDs) are expected to see a number of changes, increasing complexity. The possibility of either deemed payments or capacity payments are both under consideration. These payments would compensate a CfD asset based on its potential to produce or its installed capacity, rather than its actual power generation and market activity. This approach would decouple subsidy payments from the asset's direct performance. The process of defining the methodology, especially within the context of locational pricing, will be essential and is likely to receive significant attention in responses.

The main aim here is to ensure that a CfD doesn't create perverse signals to generators as the system becomes more renewables dominant, and also to remove the additional risks that come with that. For example, when there are so many renewable generators connected to the system that it outstrips demand, some CfD plants may not find a buyer for their day ahead volume and thus not be able to hedge to the CfD mechanism.

Implications for Energy Retailers

Much remains up in the air, given the consultation period will remain open until the 7th of May, with policy development unlikely to conclude until mid-2025. Nonetheless, it is looking very likely that locational pricing will be introduced in some form, bringing a potential new challenge to pricing teams.

We have seen time and again that current solutions for calculating prices or PPAs are simply not able to deal with the level of complexity involved, leading to slow processes or inaccuracy and lost margin. Adding in location data to calculations is yet another requirement on top of this. The predicted growth in renewable supply will mean the market for buying PPAs will expand rapidly over the coming decade, and few solutions are equipped to add differences in local wholesale prices. It’s the same story when it comes to offering prices to your I&C customers, which will now see overhauled pricing models in order to incorporate the coming changes.

Read further

Gorilla launches a pre-billing calculation layer for I&C energy contracts

More than 90% of European energy executives claim their margin reporting is accurate – but new research reveals “Margin Confidence Paradox”